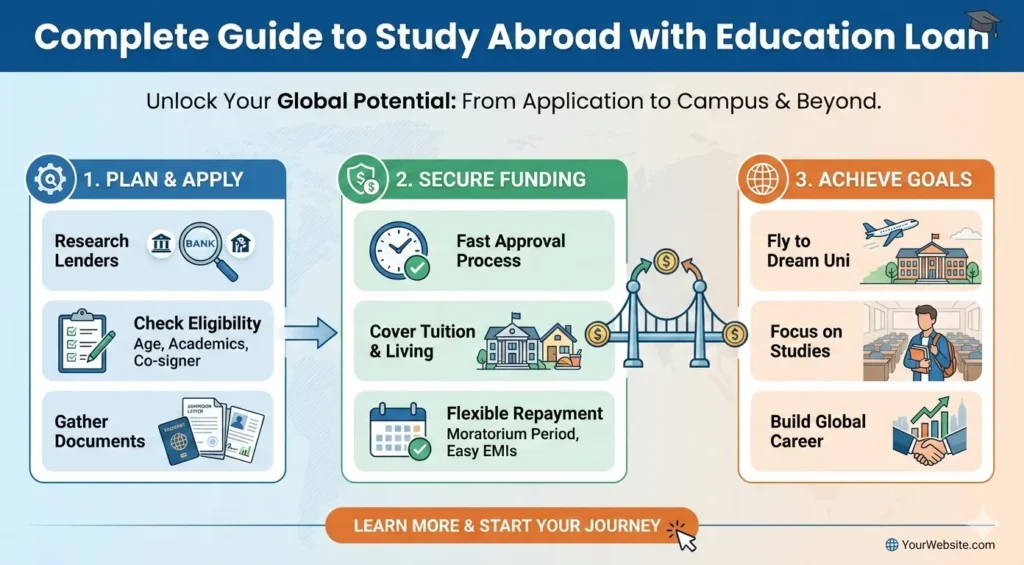

Comprehensive Comparison of Education Loan in India (for banks and NBFCs), based on the latest available data in 2025–26. This will help you pick the right lender depending on interest rate, fees, flexibility, eligibility, and other benefits.

🎓 1. Interest Rate Comparison (Banks vs NBFCs)

Banks (especially public sector):

- Typically offer lower interest rates (8.5% – ~12% p.a.), especially for public sector banks (SBI, PNB, BoB, Canara, etc.)

- Interest rates are often linked to benchmarks like MCLR/Repo + spread, meaning they can adjust with RBI policy.

NBFCs (private lenders specialized in education loans):

- Generally have higher interest rates vs banks, often in the 11% – 14.5% p.a. range, and in some cases even up to ~16%+ for certain products.

- Rates may vary significantly by profile, course, and destination (India vs abroad).

| Lender Type | Typical Rate (p.a.) | Notes |

| Public Sector Banks | ~8.5% – 11.5% | Slightly higher than the pub sector; faster processing. |

| Private Banks | ~10% – 13.5% | Slightly higher than the pub sector; faster processing. |

| NBFCs | ~11% – 14.5%+ | Higher rates but flexible terms; some offer larger unsecured amounts. |

📊 2. Loan Amount & Collateral

Banks:

- Loans can go up to ₹1.5 crore or more for studies abroad with collateral.

- Collateral is usually required above a certain threshold (e.g., loans > ₹7.5 lakh).

NBFCs:

- Loan amounts vary by provider, typically ₹40–₹80 lakh+, and some offer up to ₹2 crore in special cases.

Many NBFCs offer no or minimal collateral requirements, making them attractive for students without property.

💸 3. Other Cost Components

Processing Fees:

- Banks: Usually lower (0.5%–2% of loan amount; sometimes fixed small fees).

- NBFCs: Often higher (1.5%–2.5%+), and sometimes non-refundable.

Margin Money:

- Banks often require a student contribution (margin)—e.g., 5–15% depending on loan size/destination.

- NBFCs may offer 100% funding without margin money in many cases.

Processing Time & Documentation:

- Banks: Longer processing (2–3 weeks or more).

NBFCs: Faster (5–10 working days) and less paperwork.

🧾 4. Tax & Subsidy Benefits

Tax Deduction (Section 80E):

- If you take a bank education loan, the interest paid qualifies for deduction under Section 80E (no cap on amount, up to 8 years).

- For NBFCs, tax deductions apply only if the NBFC is notified under Sec 80E by the CBDT (less common).

Government Subsidies: Subsidies (e.g., CSIS) and schemes like PM Vidyalaxmi are offered mainly through banks, not NBFCs

🧠 5. How to Choose Based on Your Needs

Choose a Bank Loan if:

✅ You want lower interest and subsidies/tax benefits.

✅ You have or can provide collateral.

✅ You prefer regulated, traditionally strong lenders. Choose an NBFC Loan if:

✅ You need fast processing and minimal documentation.

✅ You want higher unsecured amounts without collateral.

✅ You have a less conventional course or institute abroad.

📌 Practical Examples (Indicative)

Banks

- State Bank of India: ~8.05%–11.75% p.a.; nominal processing fee on smaller loans.

- Punjab National Bank (PNB): ~9.20%+; potential concessions for females.

NBFCs

- HDFC Credila: ~9.95% – 13.25%; focused on study-abroad loans.

Avanse: ~10% – 16.5%; flexible repayment options.

Below is a side-by-side comparison of leading education loan options (Banks vs NBFCs) in India for 2026 — especially useful if you want to compare interest rates, loan amounts, processing fees, and key features before choosing a lender. (Rates and features are indicative and depend on profile, course, location, and lender policies — always verify with the bank/NBFC before applying.)

🎓 Education Loan Comparison — Banks vs NBFCs

🏦 Public & Private Banks (Lower Rates, Government-Linked)

| Bank | Interest Rate (Approx p.a.) | Max Loan Amount | Processing Fee | Key Notes |

| State Bank of India (SBI) | ~8.4% – ~11.1% | Up to ~₹1.5 Cr | Nil/Low (up to ₹10k) | Concession for girls; popular for studying abroad & India. |

| Punjab National Bank (PNB) | ~7.5% – ~10.25% | ~₹1 Cr | ~Nil – 1% | Subsidised under PM Vidyalaxmi for eligible students. |

| Bank of Baroda (BoB) | ~8.6% – ~10.2% | ~₹1 Cr+ | Nil / ~1% above threshold | Competitive for both India & abroad studies. |

| HDFC Bank | ~9.5% – ~13.5% | ~₹40 L | ~1% | Flexible repayment; faster processing than PSU banks. |

| ICICI Bank | ~9.8% – ~14% | ~₹50 L – ₹1 Cr | Up to ~2% | Unsecured options for smaller amounts. |

| Axis Bank | ~13.7% – ~15.2% | ~₹50 L + | ~2% | Higher side, but quicker sanction times. |

| Canara Bank | ~8.0% – ~11.3% | ₹40 L – higher | Nil/Low | Good concession options for meritorious students. |

| IDBI Bank | ~8.5% – ~11.1% | Varies | ~1% | No prepayment charge. |

| Union Bank of India | ~8.5% – ~12.5% | ₹40 L+ | Nil | Concession for girls; popular for studying abroad & in India. |

✅ Pros (Banks)

• Generally, lower interest rates and subsidies are available.

• Some offer tax savings (Sec 80E) and government schemes like Vidyalaxmi/Padho Pardesh. (Govt-linked, benefits apply per eligibility)

• Better for higher loan amounts with collateral. ⚠️ Cons (Banks)

• Processing time can be longer (2–4+ weeks).

• More documentation and stricter credit criteria.

📊 NBFCs (Non-Bank Finance Companies) – Flexible but Usually Costlier

| NBFC / Financier | Interest Rate (Approx p.a.) | Max Loan Amount | Processing Fee | Features |

| HDFC Credila | ~11.5% – ~13.5% | ~₹80 L+ | 0.5% – 2% | Specialist in study abroad. |

| Avanse Education | ~12.5% – ~13.5% | ~₹60 L | 0.5% – 2% | Flexible repayment; partial EMIs. |

| InCred Education | ~12.5% – ~13.5% | ~₹65 L | 0.5% – 2% | Unsecured options; simplified docs. |

| Auxilo | ~12.5% – ~13.5% | ~₹50 L | 0.5% – 2% | Customised loans; quick turnaround. |

| Bajaj Finance | ~13% – ~15% | ~₹50 L | 1% – 2% | Widely available but costlier. |

| Tata Capital | ~11.5% – ~12.75% | ~₹75 L | ~1% + GST | Competitively priced for larger unsecured amounts. |

| Muthoot Finance / Shriram Finance | ~11% – ~14% | ~₹25–30 L | 0.5% – 2% | Shorter tenures; simpler underwriting. |

✅ Pros (NBFCs)

• Usually faster approval and disbursal.

• More flexible eligibility — good if collateral or co-applicant options are limited.

• May offer interest during course payment options. ⚠️ Cons (NBFCs)

• Higher interest rates and fees are usually higher than those of banks.

• Not all NBFC loans qualify for tax benefits or government subsidies under Sec 80E.

• RBI has taken action on some lenders for non-compliance or high pricing.

📌 Quick Reference – Interest + Fees at a Glance (Indicative)

| Category | Interest Range (p.a.) | Typical Processing Fee |

| PSU Banks (e.g., SBI, PNB, BoB) | ~7.5% – ~11.5% | Nil – Low (₹0–₹10k) |

| Private Banks (e.g., HDFC, ICICI) | ~9.5% – ~14% | Moderate (1%–2%) |

| NBFCs | ~11% – ~15%+ | ~0.5% – ~2% |

🔍 Choosing the Right Option

📍 For Study in India

- If you want the lowest cost → PSU banks like SBI, PNB, BoB are often best.

- For faster processing or flexible terms → Private banks or NBFCs.

📍 For Study Abroad

- Banks can finance larger loans with collateral (up to ₹1.5 Cr).

- NBFCs are good when you need quicker disbursal or no/low collateral.

🧠 Tips Before Applying

✔ Ask lenders for the APR (annual percentage rate) — interest + all fees.

✔ Check moratorium & simple interest policies (how interest is charged during study).

✔ Ask about tax benefits (Sec 80E) and government subsidy schemes like Vidyalaxmi/Padho Pardesh.

✔ Negotiate processing fee & rate — lenders sometimes adjust based on profile.

📍 Final Tips Before You Apply

✔ Compare APR (which includes interest + all fees), not just headline rate.

✔ Check forgiveness/subsidy eligibility (banks often win here).

✔ Ask for all charges in writing (processing, insurance, pre-payment).

✔ Consider using a loan comparison/aggregator platform for customized quotes.